by Neil Da Costa | Nov 23, 2020 | Uncategorized

Lifetime gifts can either be to individuals (potentially exempt transfers) or trusts (chargeable lifetime transfers) . PETs are only taxable if the donor dies within 7 years while CLTs are taxed immediately at 20%. The attached article explains the inheritance tax...

by Neil Da Costa | Nov 22, 2020 | Uncategorized

Gains on business buildings can be postponed if the sale proceeds are reinvested in a replacement asset. Most tax exams will include questions on rollover relief and the article explains it very simply. Once you have understood the mechanics of rollover relief, you...

by Neil Da Costa | Nov 21, 2020 | Uncategorized

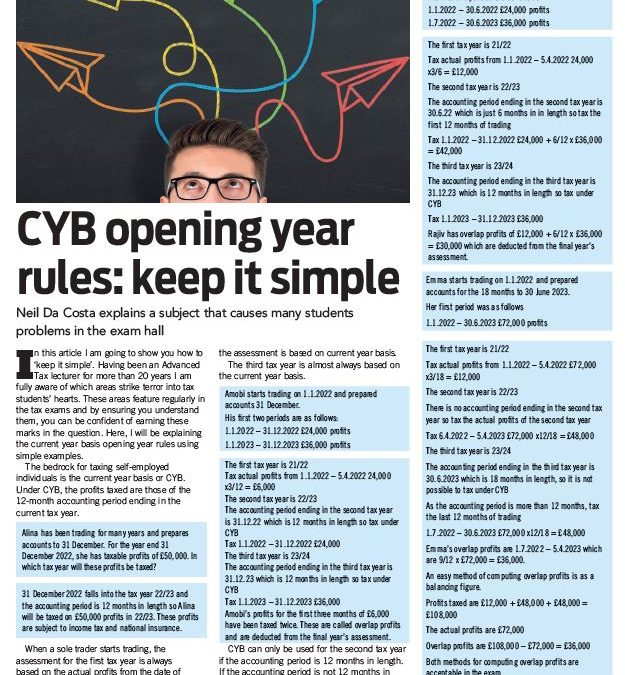

Many tax students struggle with the CYB Opening Year rules for unincorporated businesses (sole traders and partnerships). The important principle is to distinguish between the tax year and the accounting period. In this article, I have kept it simple. Remember that...

by Neil Da Costa | Nov 18, 2020 | Uncategorized

Check out my article on page 35 of the December Issue of PQ Magazine on group relief. This is a popular area with tax examiners and once you know how to identify a loss group and allocate trading losses, you will be able to pick up easy marks.

Recent Comments